TRS Passport Funds Underperform Over Last 10 Years

TDA investment options cost members hundreds of thousands in lost returns

The Spring edition of In Service News, the NYC TRS semi-annual newsletter, was recently published. The publication includes annualized returns of the seven NYC TRS Passport Funds as of December 31, 2025. The data is disappointing to say the least. It opens the door to a lot of questions and reinforces the need to resume the 8.25% fixed rate of return that was in place until 2009, and is still enjoyed by all non-UFT members.

As many are familiar, in addition to a regular pension, TRS members can choose to invest in a Tax-Deferred Annuity (TDA), also known as a 403(b) plan. Investment in the TDA is optional and TDA contributions are in addition to mandatory pension payroll deductions (mandatory pension deductions are about 6% of annual salary for a typical Tier 6 teacher). The TDA works similarly to an IRA with some additional restrictions. Among them, members are limited to seven investment options and moving money between investments or adjusting allocation of new contributions among them requires advance notice of between 30 days and up to 4 months.

Members contributing to the TDA have the choice to invest money in any combination of a fixed return fund and six market-driven investment funds. The fixed return fund earns 8.25% annually for all NYCTRS members, except UFT titles. UFT titles, including teachers, earn a reduced 7.00% (reduced from 8.25% in 2009).

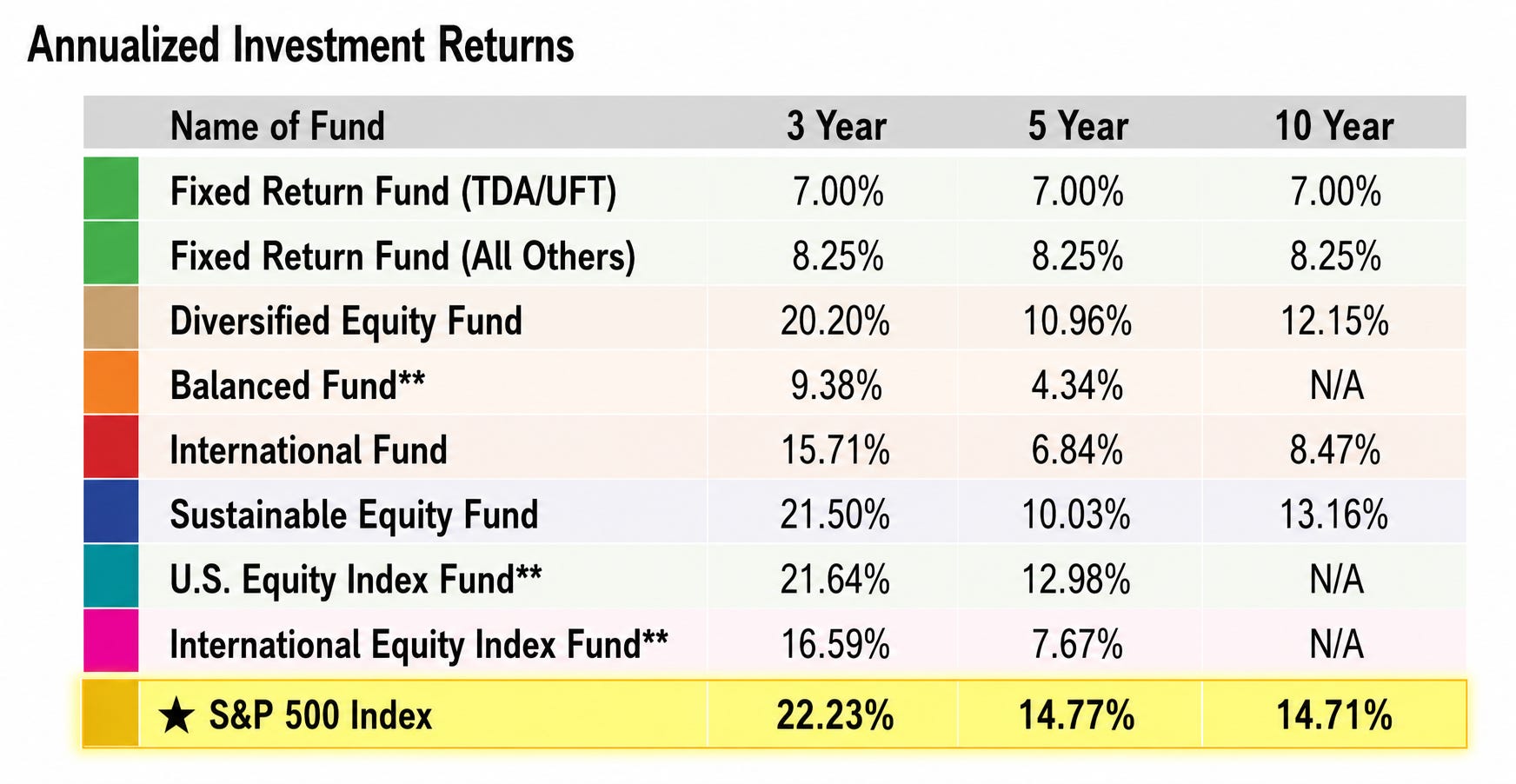

The TRS newsletter reports that all seven TRS funds underperformed the market over the 3, 5, and 10 year periods ending December 31, 2025, most by a wide margin. The 5-year annualized return on the six market-driven TRS Passport Funds was between 4 and 13%. Over the same period, the S&P returned 14.77% annually, significantly more than any of the passport funds (and more than double the UFT fixed rate of return). Over the last 10 years, the three Passport Funds that have existed for at least that amount of time, returned between 8 and 13% annually, compared to nearly 15% for the S&P 500 over the same period. The chart below shows how the TRS fund returns compare to the S&P 500.

Comparison of TRS Passport Funds to S&P 500 Index Returns

TRS Passport Funds underperformed the Market over the last 10 years.

**10 year returns unavailable for the three funds that are new within the last 10 years.

Note: The S&P 500 Index is NOT one of the investment options for TRS members. Teacher members can choose to invest their TDA savings in any combination of the seven other funds appearing in the list above (the Fixed Return Fund (UFT), and the six market-driven funds that appear below it).

Sources: TRS Passport Fund returns from TRS NYC In-Service News, Spring 2026 edition. S&P 500 returns from www.ofdollarsanddata.com

The bottom line: all seven investment options offered by TRS have underperformed the market over the last 10 years, and did so by a wide margin. The Balanced Fund returned just 4% annually, less than a quarter of the S&P 500, and the UFT fixed return fund, at 7%, returned less than half the S&P.

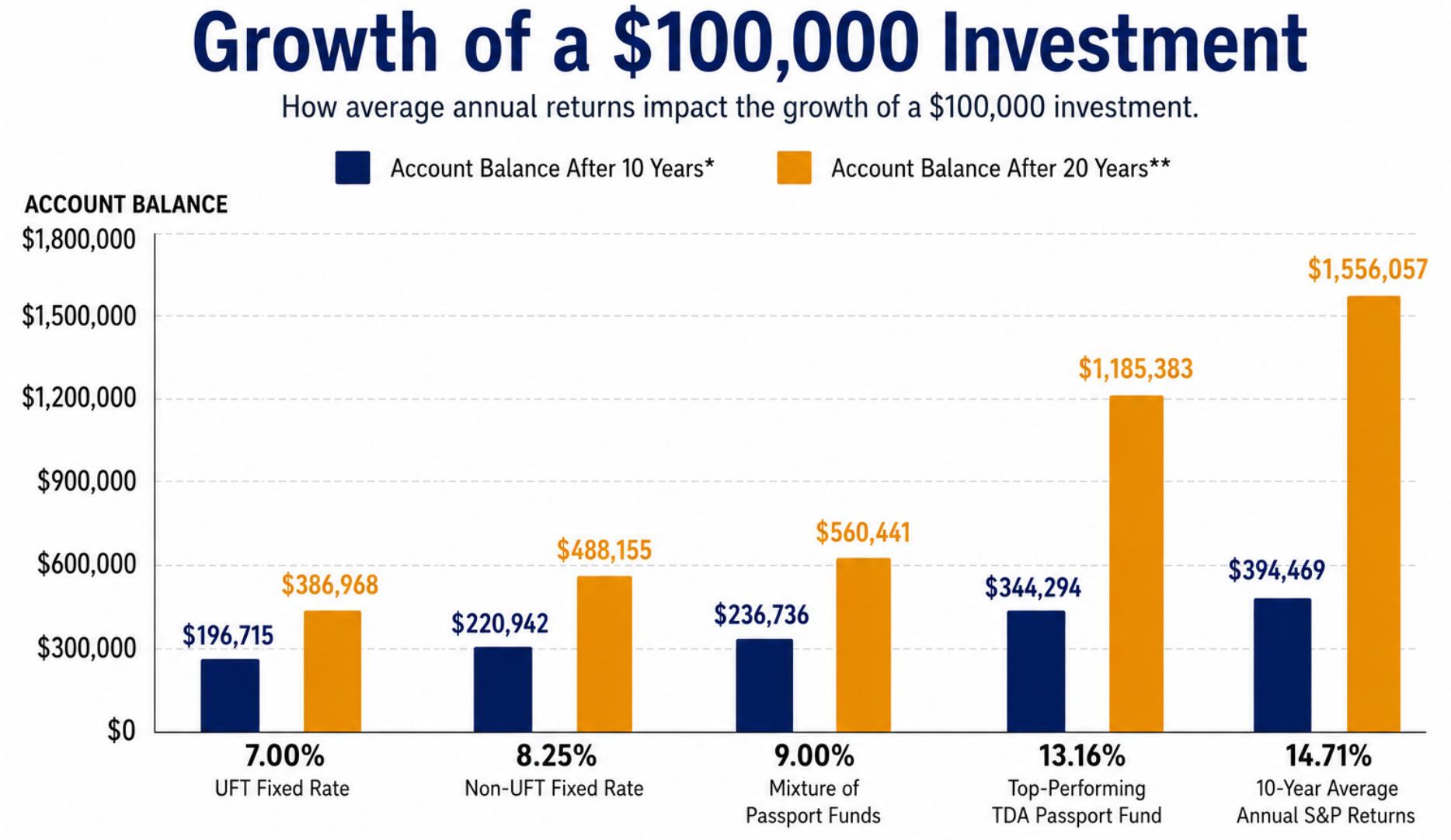

Here’s what it costs you. Suppose in 2016, you had $100,000 in your TDA account invested in a combination of passport funds earning an average annual return of 9%. Today, you would have about $237,000 if you made no additional contributions, a little more than double your savings. Had the money instead been invested in the S&P 500, it would be worth nearly $400,000, quadruple your savings, even with no additional investment.

If the pattern continues for the next 10 years, at the end of 2035, that $100,000 invested in the S&P would be worth $1.6 million, while the same money earning 9% in a mixture of TDA funds would be worth just $560,000. Even the top-performing Passport Fund, at 13.2%, would return $370,000 less than the S&P at 14.7%. The chart below shows how these returns impact your retirement savings.

*Based on historical average annual returns for the 10-year period ending 12/3125

**Based on extrapolation of average annual returns from 10-year period ending 12/31/25

Sources for Historical Returns: TRS Passport Fund returns from TRS NYC publication, In-Service News, Spring 2026 edition. S&P 500 returns from www.ofdollarsanddata.com

If I hired someone to manage my money, and they underperformed the market by that much over an extended period, I would have to ask myself why I trusted that person in the first place.

One of the advantages of a TDA compared to a traditional IRA or 401(k) is access to the Fixed Return Fund, which offers a “risk-free” fixed rate of return.

But the TDA also comes with some restrictions that don’t exist for most traditional retirement accounts, including a delay of up to four months for moving money between funds, a limited selection of funds to invest in, and additional restrictions on withdrawing funds prior to retirement.

One naturally expects the market, for which investment includes risk, to outperform a risk-free rate of return in the long run. But when none of the investment options offered by TRS even keeps up with the market, and most don’t even come close, we should be asking questions of TRS through our elected members of the Board of Trustees. At a minimum, we should be demanding to renew the 8.25% fixed rate of return still enjoyed by all other NYCTRS unions.

Disclaimer: The information contained in this article is provided for educational and informational purposes only and should not be construed as financial or investment advice. I am not a financial planner or financial advisor. The views expressed are my own and are not intended as recommendations to buy, sell, or hold any particular security, investment, or financial product. Financial decisions should be made based on your individual circumstances, objectives, and risk tolerance, and readers are encouraged to consult a qualified financial professional before making any investment or financial decisions.

I am a full-time NYC Public School teacher. I make every possible effort to fact-check my writing, but some mistakes are inevitable. If you find any errors or typos, I would be grateful if you could kindly notify me. I am indebted to friends and colleagues for their feedback on this article.